As of today, July 13, 2026, Albertans can legally play with dozens of private online casinos and sportsbooks for the first time. The province has switched on a regulated, competitive iGaming market — the second in Canada after Ontario — ending the era when the government-run PlayAlberta was the only legal option.

That is the headline. The more useful story is how Alberta got here, how its rulebook compares to Ontario and the big US markets, who actually showed up on day one, and what the next 12 months are likely to hold.

What actually happened today

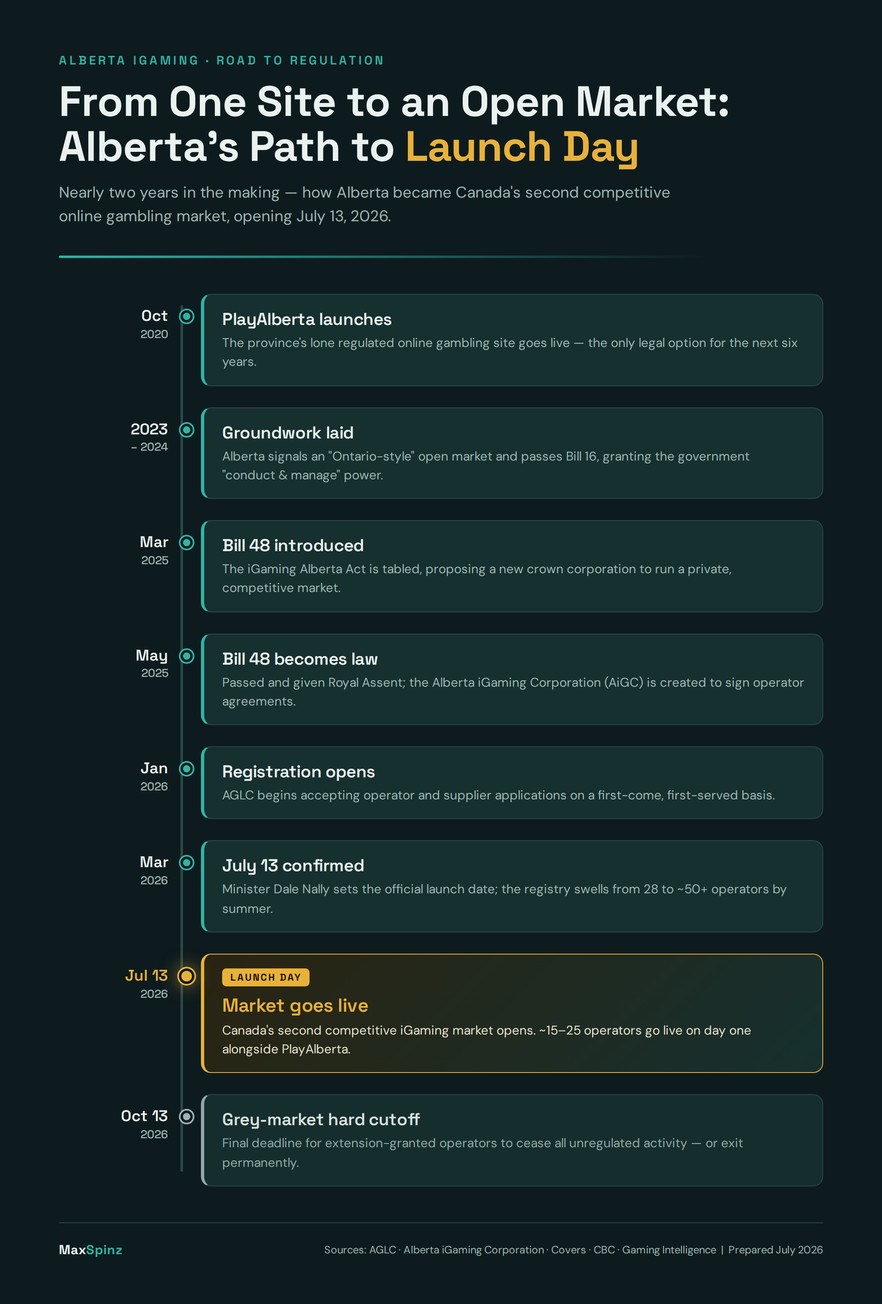

From today, private operators that have cleared two separate approvals can legally take real-money bets from Alberta residents: a registration with the Alberta Gaming, Liquor and Cannabis Commission (AGLC), and a commercial agreement with the newly created Alberta iGaming Corporation (AiGC). The market went live in the early hours of July 13, with AGLC confirming systems were a go.

For players, the practical change is choice. Until today, PlayAlberta was the province’s only regulated online casino and sportsbook; from now on it is one option among dozens. The legal gambling age stays at 18, and everyone playing must be physically located in Alberta.

The structure is lifted almost directly from Ontario: AGLC is the regulator that vets operators and enforces the rules, while the AiGC is the Crown corporation that holds the “conduct and manage” commercial agreement each operator needs before it can accept a single wager. The legal foundation is the iGaming Alberta Act (Bill 48), which received Royal Assent on May 15, 2025.

A few rules make Alberta distinctive from day one:

- Revenue split: operators keep 80% of revenue and the province takes 20%. Before that split, 3% of gross gaming revenue is carved out — 2% for First Nations as an economic-reconciliation commitment, and 1% for responsible-gambling research and treatment. That puts the effective provincial share near 22%.

- Fees: a $50,000 CAD one-time application fee, plus $150,000 a year for every brand an operator runs.

- Centralized self-exclusion from launch: a player can block themselves from every licensed online platform and land-based venue in a single registration — something Ontario took years to deliver.

- Tight advertising rules: athletes, active or retired, cannot promote specific bets or games, and public advertising of bonuses is banned outright.

- Election betting is banned, and every operator must integrate with the province’s self-exclusion system and meet strict geolocation and identity-verification standards.

The government’s motive is blunt: capture tax revenue and shrink a grey market it estimates accounts for roughly 70% of online gambling activity in the province today.

How Alberta got here — the road to launch

Alberta’s launch was years in the making.

Alberta vs Ontario: a near-copy with sharper edges

Alberta didn’t reinvent the wheel — officials openly modelled the framework on Ontario’s, which opened in April 2022. But the differences matter.

| Ontario | Alberta | |

|---|---|---|

| Launched | April 4, 2022 | July 13, 2026 |

| Regulator / commercial agency | AGCO / iGaming Ontario (iGO) | AGLC / Alberta iGaming Corp. (AiGC) |

| Minimum age | 19 | 18 |

| Government’s cut | ~20% revenue share | ~20% (~22% effective after carve-outs) |

| Annual operator fee | ~$100,000 | $150,000 per brand |

| Population | ~15–16 million | ~4.8 million |

| Athlete ad ban | Added Feb 2024, ~2 years post-launch | Built in from day one |

| Central self-exclusion | Delivered years after launch | Live from day one |

The headline takeaways: Alberta went with a lower playing age (18 vs 19), a slightly higher effective government take once the First Nations and responsible-gambling carve-outs are counted, and a higher per-brand fee — but it also launched with consumer-protection guardrails (day-one athlete-ad restrictions and centralized self-exclusion) that Ontario had to bolt on years later. Alberta, in other words, appears to have learned from Ontario’s stumbles.

The scale gap is the sobering part. Ontario reached roughly CAD $1.4 billion in iGaming revenue in its first year and only crossed CAD $4 billion in its fourth, on the back of a population more than three times Alberta’s. Alberta starts from a much smaller base — which shapes every revenue projection below.

Alberta vs the big US markets

Zoom out to North America and Alberta’s model looks distinctly Canadian. Where the US runs a fragmented, state-by-state patchwork with 21-and-up age limits and widely varying tax rates, Canada channels every private operator through a single provincial Crown agency — a structure the Criminal Code effectively requires.

| Market | Launched | iGaming tax | Min. age | 2025 iGaming rev. |

|---|---|---|---|---|

| New Jersey | 2013 | 19.75% | 21 | ~$2.9B |

| Michigan | 2021 | 20–28% (graduated) | 21 | ~$2.9B |

| Pennsylvania | 2019 | 54% on slots | 21 | ~$2.8B |

| West Virginia | 2020 | 15% | 21 | ~$331M total |

| Alberta | 2026 | ~20% (~22% eff.) | 18 | TBD |

Three things stand out for an Alberta reader. First, age: US markets are uniformly 21-plus, while Alberta plays at 18. Second, tax: Alberta’s ~20% government share is moderate — far below Pennsylvania’s 54% slots rate, and roughly in line with New Jersey’s recently raised 19.75%. That relatively operator-friendly rate is likely one reason major brands are keen; PENN Entertainment CEO Jay Snowden told investors “Canada is going to be our strongest margin market in North America.” Third, scale: each of these US states is already a multi-billion-dollar market built over 5–12 years — a reminder that Alberta’s ~4.8 million people put a natural ceiling on how big this can get.

Who showed up on day one, and how they’re playing it

Here’s the honest picture, because it matters: the market is open, not finished. By launch week, roughly 50 operators had completed AGLC registration, representing 50-plus consumer-facing brands. But registration is only half the job — each operator also needs a signed AiGC commercial agreement before taking a bet. AiGC CEO Dan Keene estimated 15–25 operators would actually be live alongside PlayAlberta on day one, with the rest phasing in over the following weeks.

The confirmed day-one names read like a who’s-who of North American gaming: FanDuel, DraftKings, BetMGM, Caesars, bet365, BetRivers, theScore Bet, PointsBet, Bet99, Betway and Sports Interaction, alongside the incumbent PlayAlberta.

The local approach comes down to two strategies. The first is multi-brand shelf-stacking: because Alberta charges per brand, the biggest operators are paying to field several at once. DraftKings launched its flagship app and Golden Nugget Online Gaming together; PENN Entertainment brought both theScore Bet and Hollywood Casino; and Super Group’s Cadtree fielded Betway plus four separate online casinos, including the well-known Spin Casino.

The second is a genuinely local, land-based-anchored play — though much of it arrives after day one. Kambi signed a multi-year deal to power Pure Casino Entertainment’s retail sportsbooks across its Alberta venues in Calgary, Edmonton and Lethbridge, with an online brand, PureCasino.ca, to follow once the market is open. First Nations-linked operators are in the mix too: Indigenous Gaming Partners and River Cree iGaming — the latter tied to Enoch Cree Nation’s River Cree Resort and Casino, west of Edmonton — hold approvals and plan to bring their platforms online later in 2026, pairing existing casino operations with new digital brands. It’s a fitting echo of the framework’s built-in First Nations revenue share.

Not everyone stayed. Coolbet pulled out entirely, ceasing Alberta operations on July 12 — the day before launch, and its second exit from a newly regulated Canadian market after leaving Ontario in 2023. It’s a reminder that “registered” and “live” are not the same status, and that the compliance bar is real. The list of available licensed apps is expected to grow over the coming weeks rather than arrive complete today.

What to expect over the next 12 months

- More brands, phasing in. Expect the live-operator count to keep climbing through late 2026 as the remaining registrants finalize their AiGC agreements — mirroring Ontario, which grew from roughly 12–16 operators at launch to about 45 within a year.

- A wide range of revenue outcomes. The government’s year-one estimate is a conservative ~CAD $76 million in tax revenue (implying roughly $390 million in gross gaming revenue). Citizens JMP Securities projects Alberta could become North America’s 8th-largest gaming market at US$700 million-plus by year three, and H2 Gambling Capital models CAD $1.9 billion by 2030.

- An immediate World Cup catalyst — with a catch. The launch lands at the end of the tournament, with the FIFA World Cup final on July 19, handing newly live sportsbooks a large acquisition moment. The catch: because registration deadlines fell late and Alberta’s offshore leakage runs high, a chunk of peak tournament betting likely already flowed to grey-market sites.

- A slow grind on channelization. The AiGC wants 70% of activity on regulated platforms in year one — reversing a market where an estimated 70% currently sits offshore — rising to 75% in year two, ambitious given how entrenched offshore play is. Ontario, for comparison, is now estimated above 91%.

- A defended incumbent. PlayAlberta isn’t going anywhere. Like Ontario’s OLG, which still holds around 20% share against 50-plus competitors, the government platform will lean on its “proceeds stay in the province” pitch to hold its ground.

Bottom line: Alberta enters with a proven template, deep operator interest, day-one player protections Ontario took years to build, and a large grey market to convert. The ceiling is real — a province of 4.8 million will never be Ontario, let alone New Jersey — but for operators eyeing one of the more operator-friendly tax regimes in North America, Alberta is a small market drawing outsized interest.

What it means for players

For Albertans, the change is less about new games and more about who stands behind them. On a licensed operator, deposits, withdrawals, self-exclusion and dispute resolution now sit under provincial oversight rather than an offshore jurisdiction. The centralized self-exclusion and deposit- and time-limit tools were in place at launch, not bolted on later — a deliberate lesson learned from watching other markets.

The rollout is gradual rather than complete. More licensed brands are due to come online over the following weeks, on top of the familiar names already live at launch. The practical marker of a licensed site is its AGLC registration: operators without one sit outside the province’s oversight, and outside the player-protection tools that come with it.

18+. Play within your limits. If gambling is a problem, support is available in Alberta: contact GameSense by AGLC at 1-833-447-7523, or call the Alberta Health Services 24-hour helpline at 1-866-332-2322.

Frequently asked questions

When did Alberta’s regulated iGaming market launch?

In the early hours of July 13, 2026. Alberta became the second Canadian province, after Ontario, to run an open market with multiple licensed private operators.

Who regulates online gambling in Alberta?

Two bodies. The AGLC (Alberta Gaming, Liquor and Cannabis Commission) is the regulator that registers and oversees operators. The Alberta iGaming Corporation (AiGC) is the Crown entity that signs the commercial agreements operators need to go live.

What is the legal gambling age in Alberta?

18 — lower than Ontario’s 19 and every regulated US state’s 21. Players must also be physically located in Alberta.

How is Alberta different from Ontario?

The architecture is similar, but Alberta is about a third of Ontario’s size, plays at 18 rather than 19, charges $150,000 per brand, and takes a 3% carve-out off gross gaming revenue (2% First Nations, 1% responsible gambling) before an 80/20 split. It also launched with athlete-ad limits and centralized self-exclusion that Ontario added years later.

Which operators are live in Alberta?

Roughly 50 operators are registered, though the AiGC estimated only about 15–25 were ready to take customers on launch day. Confirmed day-one names include FanDuel, DraftKings, BetMGM, Caesars, bet365, BetRivers, theScore Bet, PointsBet, Bet99, Betway and Sports Interaction, alongside PlayAlberta.

Is offshore online gambling still allowed in Alberta?

The point of the regulated market is to move players onto licensed platforms. Transitional tolerance for grey-market operators is generally not expected to extend past mid-October 2026, after which enforcement is expected to tighten.